Moors' Law is Murder for Motorists

Clayton Hallmark | 20.08.2012 19:31 | Climate Chaos | Energy Crisis | Technology | World

Moore's Law for transistor count is ending, but now there's Moors' Law for oil and it says gasoline -- US national average -- will be $7 in 2017 as oil reaches $120 a barrel. The law is named for Kent Moors, a professor Duquense U. Specifically, the price of oil and the number of cars in China, which drives it, double every 5 years. These murderous prices change everything in society.

Moors' Law for Oil and China's Cars

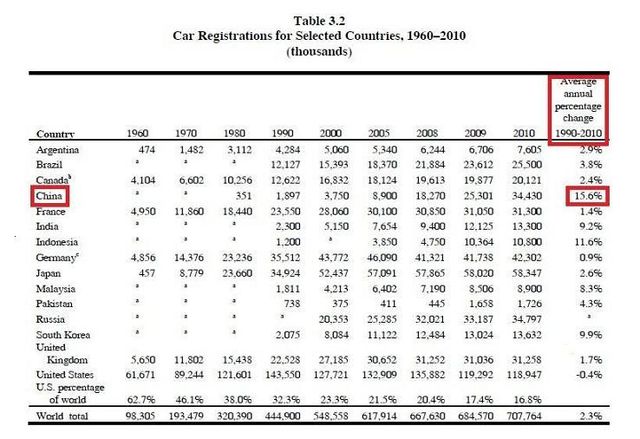

Car Registrations, Various Countries--China's doubling every 5 years

Going Viral: Moors' Law for Oil says $7 a gallon gasoline in '17

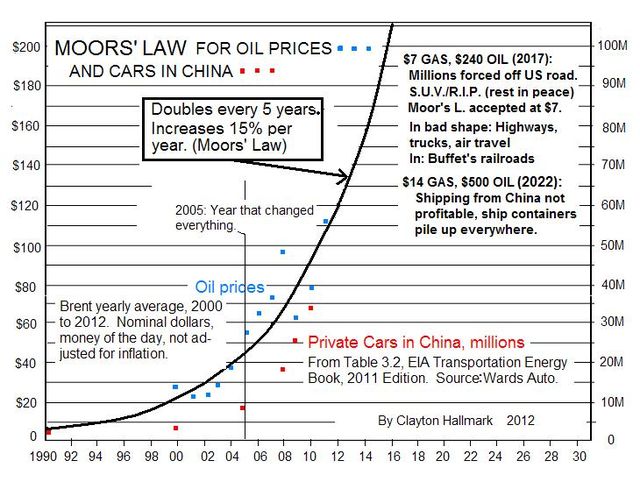

Moors' LAW FOR OIL PRICES: (Kent Moors):

"The price of oil doubles every 5 years with the doubling of automobiles in China." Moors' Law means $7 dollars a gallon gasoline, AVERAGE, in 2017 – higher, as usual, in the largest cities.

Why, and what will that do to you and me?

The graph tells the story and the table data back it up. Seven-dollar-a-gallon gasoline means millions of Americans will have to get off the road, and millions in China will take their place. China must increase and we must decrease: Econonomic activity, like heat, goes from hot to cold areas -- it's no one's fault though politics affect its, as do capital flows in the same direction to pursue opportunity (see Yanis Varoufakis).

The smooth, idealized black curve in the chart shows the trend of oil prices and China's automobile fleet, both increasing by approximately 15 percent per year, meaning a doubling in 5 years.

The price of gasoline is the price of oil per gallon (42 gal. to a barrel) plus approximately one dollar for refining, taxes, transportation, etc. -- a very reliable rule of thumb. With oil at $240 a barrel, oil would be $5.71 a gallon and, adding one dollar, the gasoline only about 5% less than $7. The gas pain is the same.

The historical data points for oil prices and China cars, which are plotted in blue and red, generally follow the black trend line. Oil prices may deviate from the trend -- sometimes greatly and for 2 or 3 years -- but then they return to trend. They have been doing this since 2005. Oil will continue increasing at about a 15% rate as long as China's car population does, which it has since 1990, or until the present financial and world system dies.

The rate for cars in China has been more precisely 15.6% (see table). Future rates will vary around the 15% trend along with oil prices.

All this is because of Peak Oil and China rising. There once was a site dedicated to debunking Peak Oil. It is here http://peakoildebunked.blogspot.com/ . The last post was over 2 years ago, just to show you how ridiculous denial is.

http://peakoildebunked.blogspot.com/ . The last post was over 2 years ago, just to show you how ridiculous denial is.

$7 PER GALLON SOON

On the other hand, don't believe Donald Trump's threat that $7-dollar-per-gallon gasoline might happen at any time. For that to be imminent would require 240-dollar oil and some calamity like the US/Israel committing attacking Iran.

However, DO look for gasoline to violate the "cheaper after Labor Day" rule because the Brent oil fields in the UK, the benchmark for world oil prices (esp., in Europe, Asia, the Middle East, and the US East Coast), are scheduled to shut down for four weeks in September 2012 just as they did in April, when there was a "surprise" (unseasonal) price hike.

You may remember that gasoline was $1-and-something from 2000 through 2004. From 2005 through 2010, it was $2-and-something. Beginning with 2011, gasoline has been $3-and-something. There was a spike and collapse in the 2008-9 recession, but gasoline prices returned to the Moors trend as soon as the recession ended.

In August 2012, three dollars is the new floor. It might last through 2013, but soon we shall be locked into $4-and-something gas, NATIONAL AVERAGE … and isn't that something? It is just the beginning.

All of this relates to the world market for oil and to exchanges in New York and London. It's not Obama's fault and it won't be Romney's fault. The US standard for crude oil is the price of West Texas Intermediate, WTI, which is currently about $18 cheaper than Brent. WTI has meant less since the US lost dominance over world oil prices around 1970 when its own production peaked. OPEC took control in the 1970s and the Oil Shocks quickly ensued. In 2005, the Arabs lost control to the Law of Supply and Demand and Moors' Law -- nobody's in charge now and Brent is the world oil price standard

DR. KENT Moors

Kent Moors is the famous (in oil and energy circles) political science professor and financial and government-intelligence advisor, from Duquense University in Pittsburgh, and one of the most cited sources by media and scholars on oil and gasoline prices.

Moors has not explicitly enunciated any periodic increase in oil prices, but the law is based on my understanding of Moors' model for oil and gasoline prices. I have named the law for him much as the Caltech solid-state physics scientist Carver Mead named Moore's Law (for transistor doubling on a computer chip) after Gordon Moore, the science and business genius behind Intel. That law ended in 2006 as I predicted in a graph shown here: http://www.upm.ro/InterIng2007/Papers/Section2/13-TAUCEAN_Timisoara_1.pdf .

Moors’ model for short-term price forecasting (as opposed his law) is based on:

-- spreads between gasoline "futures contracts" (contracts for delivery at a specified future date) versus related instruments (ETFs) traded on financial exchanges;

-- differentials between oil-contract prices for different dates, oil fields, and quality;

-- refinery production runs;

-- anecdotal intelligence from acquaintances; and

-- complex-systems theory (see "limits to growth" movement and Jay Forrester and Dennis Meadows at MIT, also see end of this article).

Kent Moors has been working on this for over 35 years.

BIGGEST CHANGE TO THE SCENE SINCE THE INTERSTATE HIGHWAYS

Seven dollar a gallon gasoline is the biggest thing in Moors' field since the construction of the Interstate Highway System. It will cause the biggest visible change in the American landscape, the "made" environment -- all that you see around you outdoors -- since the Interstates. See LA in the "Bladerunner" movie to picture this. Or visit Detroit.

LAW OF SUPPLY AND DEMAND WILL NOT BE DENIED

Note the vertical line down the chart that divides it into before and after the year 2005. About Thanksgiving Day of that year (as Ken Deffeyes of Princeton wryly put it), world production of conventional crude oil -- the cheap, easy-to-get kind that Detroit and US manufacturing dominance were built on -- peaked out at about 74 mbd (million barrels per day). World oil production, with "nonconventional" sources added, has increased since then to 87 (IEA, international) or 88 mbd (US EIA figure) – but not the cheap kind of crude. Note that the graph shows oil prices assuming the Moors' Law rate in 2005 – a key date.

CARS IN CHINA VS. OIL PRICES -- CAUSAL, NOT CASUAL COINCIDENCE.

The exponential increase (periodic doubling, every 5 years) of the numbers of automobiles registered in China has been going on longer than the 5-year doubling of oil prices -- since 1990 for cars vs 2005 for oil -- so it is a cause rather than an effect. (See the table.)

The other main cause of repeated oil-price doubling is the peaking of world conventional oil (crude oil and lease condensate, a natural gas liquid that comes along with the crude) production in 2005. With the *demand*, esp. in China, increasing exponentially and the *supply* now limited for "easy" oil, there suddenly was a supply-demand imbalance in 2005 and no place for oil and gas prices to go but up. This is Econ 101.

With the end of Supply = Demand, 2005 changes everything. As Jeffrey Rubin, the former chief economist at CIBC World Markets (investment banking arm of Canadian bank CIBC), always says, "I am an economist. I believe in the power of prices." (Jeff Rubin is another forecaster to follow.)

Peak Oil 2005, combined with Chinese motorization at around 15.6% per annum, is what produced Moors' Law doubling at around 15%. Gasoline follows suit.

MOORS RULES DESPITE RECESSIONS AND A PRICE-INCENTIVE TO DEVELOP MORE OIL SOURCES

Fall in Gas Prices As in 2008-2009 Not Likely Repeated

Two-dollars-and-something gasoline seen in the 2008-2009 recession is not likely to be repeated in future crises -- even worse ones, as we all soon shall find out.

The demand versus supply of cheap oil has reached a point, in 2012, in which even deep recession in the largest and second largest economies in the world --the US and Europe -- can not overcome the increased demand for oil and gas in China.

The supply/demand imbalance after 2005 and the Moors' Law price trend it engendered will remain in place over a decade.

BAKKEN WON'T SAVE OUR BACON

The price for oil is that of the HIGHEST PRICE refiners and consumers are willing to pay drillers to extract the "LAST BARREL" that goes on the market -- the "most difficult" barrel. Forget about gushers in the Middle East or anywhere else. It's small sources like Bakken shale oil shipped on trains (Warren Buffet's) and trucks out of North Dakota that governs the market prices, and this is the hard-to-get oil.

As for cheap conventional crude oil fields (in the Middle East, Mexico, Alaska, etc.), these are depleting at the rate of about 6% a year, a loss of about 4.44 milliion barrels per day (mbd). Compare that to the 0.55 mbd of Bakken shale oil currently being produced in N. Dakota. On the world market, gains in N. Dakota are eaten up by depletion in the OPECs -- but Bakken and other “boutique” (expensive, niche) sources rule the price worldwide.

An increasing amount of oil is taken from the world's export market just by increasing use in the OPEC countries, where the stuff is practically given away. As of August 13, 2012, you can get premium gasoline in Venezuela for 9 cents a gallon! (Venezuelans must love Chavez.) Saudis pay 69 cents for premium, Kuwaitis 89 ... you get the picture. OPEC consumption is probably increasing at a rate of about 4% a year, or by about 0.7 mbd last year, 700,000 barrels. This withholding from the market effectively cancels out N. Dakota Bakken production. http://webcache.googleusercontent.com/search?q=cache:0Mo_HUsKSlcJ:www.econ.nyu.edu/dept/courses/gately/OPEC_Consumption_Gately_AlYousef_AlSheikh_April2012.pdf+oil+consumption+opec&cd=13&hl=en&ct=clnk&gl=us

Remember, the market for oil and gasoline is a world market, with prices set mainly on New York and London exchanges. The US can and does export even gasoline. Oil and gas flow to wherever the demand is, which is in China even though gasoline there is about $1 higher than in the United States. http://www.bloomberg.com/slideshow/2012-08-13/highest-cheapest-gas-prices-by-country.html#slide54

DEMAND (SEE TABLE)

The table, Car Registrations for Selected Countries, 1960-2010 (from the "US Dept. of Energy Transportation Data Book), shows where the growth in demand for cars, oil, and gasoline is.

The annual percentage change from 1990 to 2010 was 15.6 percent for China. It was 9.2 percent for the world's other really large-population country, India. For the US, the change was -0.4 percent -- the US car fleet is shrinking. Millions of cars and drivers in the US will be forced off the road by high gasoline and highway prices (privatization, tolls) .

The 15.6% China fleet growth is very close to the 15% oil-hike rate noted by UK scientist David King and explained in detail by Professor Minqi Li (sounds like "Minchi Lee") of the University of Utah.

There are complex, nonlinear (effect not proportional to cause) interactions among the correlated variables employed in Moors' price model and embedded in and simplified by Moors' Law. But as for the oil demand factor, "The growth in the World total [cars registered] comes mainly from developing countries like China, India, and South Korea," as the EIA said in the table notes.

SUMMARY

-- In oil *demand*, China's car fleet rules.

-- In *supply*, the price of the "most expensive barrel" available in quantity, wherever in the world it is, rules.

-- *Overall*, for crude-oil prices, Moors' Law and the exponential function rule.

FAQs -- FREQUENTLY ASKED QUESTIONS

WHY IS "THE EXPONENTIAL" SO IMPORTANT -- THOUGH IGNORED?

The curves in the graph describe an exponential: It doubles regularly like money lent out or borrowed at compound interest. Once established, an exponential trend, esp. in large-scale phenomena, tends to be very persistent. This one represents a doubling every 5 years of the world oil price and cars in China. If it lasted 20 years, oil would go to $1600 and gas to $40. Oil would be used to fill little All-in-One cans and to lubricate sewing machines, but not for fuel and mobility.

Oil at $800 per barrel (due within 15 years), however, is conceivable, and journalist Christopher Steiner wrote a New York Times Bestseller on the results. It is titled "$20-Per-Gallon" and based partly on data from economist Jeff Rubin.

I will have hope for the people of the United States when they understand the exponential and its meaning in life. Albert Einstein - "Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it." Obama and Romney don’t “get it.”

The other main thing to understand about an exponential function is that it must end sometime.

JUST HOW LONG AND HOW FAR WILL ALL OF THIS GO?

If the trends continued only 15 years -- oil over $800, gasoline above $20, and China's cars increasing at 15.6% per year -- China's car-market penetration (cars per population) would go from 58.7 per 1000 persons (2010 data) to 469.7 per 1000 in 2027. This is a reasonable plateau since already some of the largest cities in China are limiting new registrations and the US topped out at 800 per 1000 persons in 2010 and has stayed close to 800 since. (The US will stay there, and decline, since the market is saturated.) THERE MUST BE LIMITS, but Steiner's nightmares in "20-Dollars-per-Gallon" seem realistic.

In real life there are limits -- why you don't see 10-foot people, why loans end and investments end.

FROM EXPONENTIAL TO LOGISTIC (S-CURVES, OGIVES – AND LIMITS

In nature, the exponential is just the fore part of a "logistic" function and is followed by a leveling off at the end of a process so that the overall trend curve resembles the letter “S.” Sometimes the leveling-off is preceded by a bump upward at the end of the exponential rise. The leveling-off may include oscillations at a regular interval, or else chaotic (irregular) fluctuations, around the eventual level.

WORSE THAN LIMITS TO GROWTH: COLLAPSE

Finally, sometimes an exponential phenomenon decays back to a lower level in a short time: It collapses. The Limits to Growth movement (Jay Forrester, Dennis Meadows, Graham Turner, etc.) expects a convergence of declining world social and material systems (food production, etc.) -- a result of exceeding the earth's resource limits -- to lead to a worldwide collapse of the systems and a drastic decline in the world's population. The curves or trajectories of these are like a double-exponential (e.g., charge-discharge) curve with the peak rounded off.

The "standard" run of the group's World3 model, originated in the early 1970s, appears to be on track for all this. The world population would decline to the early-1970s level of 3.7 billion from the present 7 billion by around the year 2100. The implications are not good, I must say.

According to the model, impending collapse should be apparent by 2015-2025. One limit, Peak Oil, already has been reached. Peak world industrial output per capita, including China, should occur around 2015, according to the model (meaning output of developed nations must fall). Deaths should exceed births around 2025. Already the UN reports that the world mortality rate (a component of the model) is increasing.

Two components of the model are in decline now, at least in the US: Industrial output per capita and electricity production per capita.

BEYOND Moors: COLLAPSE OF CIVILIZATION? ANOTHER S-CURVE UNDER A “DISTRIBUTED CHAOS” SYSTEM AND AN OIL REPLACEMENT?

If the time to double decreased from the Moors' Law rate of 5 years to doubling in only, say, 3 or 2.5 years, the rate would be called “superexponential” (and Moors' Law, by definition, would end, just as Moore’s Law did in 2006). An example is housing prices in California, Arizona,Nevada, Florida, and New England, which increased at a superexponential rate in the bubble before the Housing Crash. This told some forecasters, e.g., Didier Sornette, a complex-systems scientist in earthquake prediction at UCLA at the time, that a collapse was imminent.

A superexponential increase is a prologue to a “phase” change, or state change, like a change from liquid water to vapor, or an explosive change from gasoline to combustion gases. Now we may be facing a societal blowup, not a mere housing or financial collapse.

My own view is that we are in the midst of a “primary-energy replacement” of the same significance as the historical ones from wood to coal and from coal to oil. Coal reached its peak share of world energy consumption around 1920, about the same time the power of the British Empire peaked and the US became the main money lender to them and other combatants of World War I, and the leading nation.

The next primary-energy replacement – oil for coal – brought an Automobile Age boom in the 1920s and a bust, the Depression, in the 1930s. Oil’s share of primary-energy production peaked around 1975. The US (about 15 years later) became hegemonic in this energy replacement (essentially the only superpower in a unipolar world), but it first had to resort to the Twin Deficits (in trade and the federal budget) financed by foreigners. The mid-1970s peak in oil’s share of world energy was associated with a shift in US employment to “knowledge” work (Lars Onsager’s “Reciprocity Relation” in physics applied to sociology”) and to a “We think, they sweat” approach to foreign trade.

After Peak Oil (affordable oil), there must be a new energy replacement, gas and nuclear energy for oil. In this current replacement, in the late 1980s, natural gas use reached and surpassed oil use. This suggests new hegemonies:

-- politically, groups like the BRICS countries, Europe, and East Asia sharing power with the US – a multipolar world – and,

-- economically, we should see employment in finance, trade, and knowledge-work returning to a lower level -- (and abandoned, “see-through,” office buildings, their ceilings falling down and parking lots taken over by weeds, following in footsteps of long-abandoned abandoned factories ).

The replacement of oil will involve cataclysmic, epic changes in human activity and the human condition – but perhaps stop short of a societal collapse. We may instead be entering an era of DISTRIBUTED CHAOS – the current chaos spreading out and playing out in a divided Europe, possibly a split-up USA (with secessions), more localism and much less world trade and even interstate trade (e.g., between US states).

The energy changes will bring much pain over many years, but distributed chaos is better than a return to precivilization -- an absence of hierarchy and reduction to the elemental units of tribe and family. In the latter, society would achieve equilibrium all right -- not the one sought for, but the societal equivalent of the “heat death of the universe.”

Clayton Hallmark

Moors' LAW FOR OIL PRICES: (Kent Moors):

"The price of oil doubles every 5 years with the doubling of automobiles in China." Moors' Law means $7 dollars a gallon gasoline, AVERAGE, in 2017 – higher, as usual, in the largest cities.

Why, and what will that do to you and me?

The graph tells the story and the table data back it up. Seven-dollar-a-gallon gasoline means millions of Americans will have to get off the road, and millions in China will take their place. China must increase and we must decrease: Econonomic activity, like heat, goes from hot to cold areas -- it's no one's fault though politics affect its, as do capital flows in the same direction to pursue opportunity (see Yanis Varoufakis).

The smooth, idealized black curve in the chart shows the trend of oil prices and China's automobile fleet, both increasing by approximately 15 percent per year, meaning a doubling in 5 years.

The price of gasoline is the price of oil per gallon (42 gal. to a barrel) plus approximately one dollar for refining, taxes, transportation, etc. -- a very reliable rule of thumb. With oil at $240 a barrel, oil would be $5.71 a gallon and, adding one dollar, the gasoline only about 5% less than $7. The gas pain is the same.

The historical data points for oil prices and China cars, which are plotted in blue and red, generally follow the black trend line. Oil prices may deviate from the trend -- sometimes greatly and for 2 or 3 years -- but then they return to trend. They have been doing this since 2005. Oil will continue increasing at about a 15% rate as long as China's car population does, which it has since 1990, or until the present financial and world system dies.

The rate for cars in China has been more precisely 15.6% (see table). Future rates will vary around the 15% trend along with oil prices.

All this is because of Peak Oil and China rising. There once was a site dedicated to debunking Peak Oil. It is here

http://peakoildebunked.blogspot.com/ . The last post was over 2 years ago, just to show you how ridiculous denial is. $7 PER GALLON SOON

On the other hand, don't believe Donald Trump's threat that $7-dollar-per-gallon gasoline might happen at any time. For that to be imminent would require 240-dollar oil and some calamity like the US/Israel committing attacking Iran.

However, DO look for gasoline to violate the "cheaper after Labor Day" rule because the Brent oil fields in the UK, the benchmark for world oil prices (esp., in Europe, Asia, the Middle East, and the US East Coast), are scheduled to shut down for four weeks in September 2012 just as they did in April, when there was a "surprise" (unseasonal) price hike.

You may remember that gasoline was $1-and-something from 2000 through 2004. From 2005 through 2010, it was $2-and-something. Beginning with 2011, gasoline has been $3-and-something. There was a spike and collapse in the 2008-9 recession, but gasoline prices returned to the Moors trend as soon as the recession ended.

In August 2012, three dollars is the new floor. It might last through 2013, but soon we shall be locked into $4-and-something gas, NATIONAL AVERAGE … and isn't that something? It is just the beginning.

All of this relates to the world market for oil and to exchanges in New York and London. It's not Obama's fault and it won't be Romney's fault. The US standard for crude oil is the price of West Texas Intermediate, WTI, which is currently about $18 cheaper than Brent. WTI has meant less since the US lost dominance over world oil prices around 1970 when its own production peaked. OPEC took control in the 1970s and the Oil Shocks quickly ensued. In 2005, the Arabs lost control to the Law of Supply and Demand and Moors' Law -- nobody's in charge now and Brent is the world oil price standard

DR. KENT Moors

Kent Moors is the famous (in oil and energy circles) political science professor and financial and government-intelligence advisor, from Duquense University in Pittsburgh, and one of the most cited sources by media and scholars on oil and gasoline prices.

Moors has not explicitly enunciated any periodic increase in oil prices, but the law is based on my understanding of Moors' model for oil and gasoline prices. I have named the law for him much as the Caltech solid-state physics scientist Carver Mead named Moore's Law (for transistor doubling on a computer chip) after Gordon Moore, the science and business genius behind Intel. That law ended in 2006 as I predicted in a graph shown here:

http://www.upm.ro/InterIng2007/Papers/Section2/13-TAUCEAN_Timisoara_1.pdf . Moors’ model for short-term price forecasting (as opposed his law) is based on:

-- spreads between gasoline "futures contracts" (contracts for delivery at a specified future date) versus related instruments (ETFs) traded on financial exchanges;

-- differentials between oil-contract prices for different dates, oil fields, and quality;

-- refinery production runs;

-- anecdotal intelligence from acquaintances; and

-- complex-systems theory (see "limits to growth" movement and Jay Forrester and Dennis Meadows at MIT, also see end of this article).

Kent Moors has been working on this for over 35 years.

BIGGEST CHANGE TO THE SCENE SINCE THE INTERSTATE HIGHWAYS

Seven dollar a gallon gasoline is the biggest thing in Moors' field since the construction of the Interstate Highway System. It will cause the biggest visible change in the American landscape, the "made" environment -- all that you see around you outdoors -- since the Interstates. See LA in the "Bladerunner" movie to picture this. Or visit Detroit.

LAW OF SUPPLY AND DEMAND WILL NOT BE DENIED

Note the vertical line down the chart that divides it into before and after the year 2005. About Thanksgiving Day of that year (as Ken Deffeyes of Princeton wryly put it), world production of conventional crude oil -- the cheap, easy-to-get kind that Detroit and US manufacturing dominance were built on -- peaked out at about 74 mbd (million barrels per day). World oil production, with "nonconventional" sources added, has increased since then to 87 (IEA, international) or 88 mbd (US EIA figure) – but not the cheap kind of crude. Note that the graph shows oil prices assuming the Moors' Law rate in 2005 – a key date.

CARS IN CHINA VS. OIL PRICES -- CAUSAL, NOT CASUAL COINCIDENCE.

The exponential increase (periodic doubling, every 5 years) of the numbers of automobiles registered in China has been going on longer than the 5-year doubling of oil prices -- since 1990 for cars vs 2005 for oil -- so it is a cause rather than an effect. (See the table.)

The other main cause of repeated oil-price doubling is the peaking of world conventional oil (crude oil and lease condensate, a natural gas liquid that comes along with the crude) production in 2005. With the *demand*, esp. in China, increasing exponentially and the *supply* now limited for "easy" oil, there suddenly was a supply-demand imbalance in 2005 and no place for oil and gas prices to go but up. This is Econ 101.

With the end of Supply = Demand, 2005 changes everything. As Jeffrey Rubin, the former chief economist at CIBC World Markets (investment banking arm of Canadian bank CIBC), always says, "I am an economist. I believe in the power of prices." (Jeff Rubin is another forecaster to follow.)

Peak Oil 2005, combined with Chinese motorization at around 15.6% per annum, is what produced Moors' Law doubling at around 15%. Gasoline follows suit.

MOORS RULES DESPITE RECESSIONS AND A PRICE-INCENTIVE TO DEVELOP MORE OIL SOURCES

Fall in Gas Prices As in 2008-2009 Not Likely Repeated

Two-dollars-and-something gasoline seen in the 2008-2009 recession is not likely to be repeated in future crises -- even worse ones, as we all soon shall find out.

The demand versus supply of cheap oil has reached a point, in 2012, in which even deep recession in the largest and second largest economies in the world --the US and Europe -- can not overcome the increased demand for oil and gas in China.

The supply/demand imbalance after 2005 and the Moors' Law price trend it engendered will remain in place over a decade.

BAKKEN WON'T SAVE OUR BACON

The price for oil is that of the HIGHEST PRICE refiners and consumers are willing to pay drillers to extract the "LAST BARREL" that goes on the market -- the "most difficult" barrel. Forget about gushers in the Middle East or anywhere else. It's small sources like Bakken shale oil shipped on trains (Warren Buffet's) and trucks out of North Dakota that governs the market prices, and this is the hard-to-get oil.

As for cheap conventional crude oil fields (in the Middle East, Mexico, Alaska, etc.), these are depleting at the rate of about 6% a year, a loss of about 4.44 milliion barrels per day (mbd). Compare that to the 0.55 mbd of Bakken shale oil currently being produced in N. Dakota. On the world market, gains in N. Dakota are eaten up by depletion in the OPECs -- but Bakken and other “boutique” (expensive, niche) sources rule the price worldwide.

An increasing amount of oil is taken from the world's export market just by increasing use in the OPEC countries, where the stuff is practically given away. As of August 13, 2012, you can get premium gasoline in Venezuela for 9 cents a gallon! (Venezuelans must love Chavez.) Saudis pay 69 cents for premium, Kuwaitis 89 ... you get the picture. OPEC consumption is probably increasing at a rate of about 4% a year, or by about 0.7 mbd last year, 700,000 barrels. This withholding from the market effectively cancels out N. Dakota Bakken production.

http://webcache.googleusercontent.com/search?q=cache:0Mo_HUsKSlcJ:www.econ.nyu.edu/dept/courses/gately/OPEC_Consumption_Gately_AlYousef_AlSheikh_April2012.pdf+oil+consumption+opec&cd=13&hl=en&ct=clnk&gl=us Remember, the market for oil and gasoline is a world market, with prices set mainly on New York and London exchanges. The US can and does export even gasoline. Oil and gas flow to wherever the demand is, which is in China even though gasoline there is about $1 higher than in the United States.

http://www.bloomberg.com/slideshow/2012-08-13/highest-cheapest-gas-prices-by-country.html#slide54 DEMAND (SEE TABLE)

The table, Car Registrations for Selected Countries, 1960-2010 (from the "US Dept. of Energy Transportation Data Book), shows where the growth in demand for cars, oil, and gasoline is.

The annual percentage change from 1990 to 2010 was 15.6 percent for China. It was 9.2 percent for the world's other really large-population country, India. For the US, the change was -0.4 percent -- the US car fleet is shrinking. Millions of cars and drivers in the US will be forced off the road by high gasoline and highway prices (privatization, tolls) .

The 15.6% China fleet growth is very close to the 15% oil-hike rate noted by UK scientist David King and explained in detail by Professor Minqi Li (sounds like "Minchi Lee") of the University of Utah.

There are complex, nonlinear (effect not proportional to cause) interactions among the correlated variables employed in Moors' price model and embedded in and simplified by Moors' Law. But as for the oil demand factor, "The growth in the World total [cars registered] comes mainly from developing countries like China, India, and South Korea," as the EIA said in the table notes.

SUMMARY

-- In oil *demand*, China's car fleet rules.

-- In *supply*, the price of the "most expensive barrel" available in quantity, wherever in the world it is, rules.

-- *Overall*, for crude-oil prices, Moors' Law and the exponential function rule.

FAQs -- FREQUENTLY ASKED QUESTIONS

WHY IS "THE EXPONENTIAL" SO IMPORTANT -- THOUGH IGNORED?

The curves in the graph describe an exponential: It doubles regularly like money lent out or borrowed at compound interest. Once established, an exponential trend, esp. in large-scale phenomena, tends to be very persistent. This one represents a doubling every 5 years of the world oil price and cars in China. If it lasted 20 years, oil would go to $1600 and gas to $40. Oil would be used to fill little All-in-One cans and to lubricate sewing machines, but not for fuel and mobility.

Oil at $800 per barrel (due within 15 years), however, is conceivable, and journalist Christopher Steiner wrote a New York Times Bestseller on the results. It is titled "$20-Per-Gallon" and based partly on data from economist Jeff Rubin.

I will have hope for the people of the United States when they understand the exponential and its meaning in life. Albert Einstein - "Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it." Obama and Romney don’t “get it.”

The other main thing to understand about an exponential function is that it must end sometime.

JUST HOW LONG AND HOW FAR WILL ALL OF THIS GO?

If the trends continued only 15 years -- oil over $800, gasoline above $20, and China's cars increasing at 15.6% per year -- China's car-market penetration (cars per population) would go from 58.7 per 1000 persons (2010 data) to 469.7 per 1000 in 2027. This is a reasonable plateau since already some of the largest cities in China are limiting new registrations and the US topped out at 800 per 1000 persons in 2010 and has stayed close to 800 since. (The US will stay there, and decline, since the market is saturated.) THERE MUST BE LIMITS, but Steiner's nightmares in "20-Dollars-per-Gallon" seem realistic.

In real life there are limits -- why you don't see 10-foot people, why loans end and investments end.

FROM EXPONENTIAL TO LOGISTIC (S-CURVES, OGIVES – AND LIMITS

In nature, the exponential is just the fore part of a "logistic" function and is followed by a leveling off at the end of a process so that the overall trend curve resembles the letter “S.” Sometimes the leveling-off is preceded by a bump upward at the end of the exponential rise. The leveling-off may include oscillations at a regular interval, or else chaotic (irregular) fluctuations, around the eventual level.

WORSE THAN LIMITS TO GROWTH: COLLAPSE

Finally, sometimes an exponential phenomenon decays back to a lower level in a short time: It collapses. The Limits to Growth movement (Jay Forrester, Dennis Meadows, Graham Turner, etc.) expects a convergence of declining world social and material systems (food production, etc.) -- a result of exceeding the earth's resource limits -- to lead to a worldwide collapse of the systems and a drastic decline in the world's population. The curves or trajectories of these are like a double-exponential (e.g., charge-discharge) curve with the peak rounded off.

The "standard" run of the group's World3 model, originated in the early 1970s, appears to be on track for all this. The world population would decline to the early-1970s level of 3.7 billion from the present 7 billion by around the year 2100. The implications are not good, I must say.

According to the model, impending collapse should be apparent by 2015-2025. One limit, Peak Oil, already has been reached. Peak world industrial output per capita, including China, should occur around 2015, according to the model (meaning output of developed nations must fall). Deaths should exceed births around 2025. Already the UN reports that the world mortality rate (a component of the model) is increasing.

Two components of the model are in decline now, at least in the US: Industrial output per capita and electricity production per capita.

BEYOND Moors: COLLAPSE OF CIVILIZATION? ANOTHER S-CURVE UNDER A “DISTRIBUTED CHAOS” SYSTEM AND AN OIL REPLACEMENT?

If the time to double decreased from the Moors' Law rate of 5 years to doubling in only, say, 3 or 2.5 years, the rate would be called “superexponential” (and Moors' Law, by definition, would end, just as Moore’s Law did in 2006). An example is housing prices in California, Arizona,Nevada, Florida, and New England, which increased at a superexponential rate in the bubble before the Housing Crash. This told some forecasters, e.g., Didier Sornette, a complex-systems scientist in earthquake prediction at UCLA at the time, that a collapse was imminent.

A superexponential increase is a prologue to a “phase” change, or state change, like a change from liquid water to vapor, or an explosive change from gasoline to combustion gases. Now we may be facing a societal blowup, not a mere housing or financial collapse.

My own view is that we are in the midst of a “primary-energy replacement” of the same significance as the historical ones from wood to coal and from coal to oil. Coal reached its peak share of world energy consumption around 1920, about the same time the power of the British Empire peaked and the US became the main money lender to them and other combatants of World War I, and the leading nation.

The next primary-energy replacement – oil for coal – brought an Automobile Age boom in the 1920s and a bust, the Depression, in the 1930s. Oil’s share of primary-energy production peaked around 1975. The US (about 15 years later) became hegemonic in this energy replacement (essentially the only superpower in a unipolar world), but it first had to resort to the Twin Deficits (in trade and the federal budget) financed by foreigners. The mid-1970s peak in oil’s share of world energy was associated with a shift in US employment to “knowledge” work (Lars Onsager’s “Reciprocity Relation” in physics applied to sociology”) and to a “We think, they sweat” approach to foreign trade.

After Peak Oil (affordable oil), there must be a new energy replacement, gas and nuclear energy for oil. In this current replacement, in the late 1980s, natural gas use reached and surpassed oil use. This suggests new hegemonies:

-- politically, groups like the BRICS countries, Europe, and East Asia sharing power with the US – a multipolar world – and,

-- economically, we should see employment in finance, trade, and knowledge-work returning to a lower level -- (and abandoned, “see-through,” office buildings, their ceilings falling down and parking lots taken over by weeds, following in footsteps of long-abandoned abandoned factories ).

The replacement of oil will involve cataclysmic, epic changes in human activity and the human condition – but perhaps stop short of a societal collapse. We may instead be entering an era of DISTRIBUTED CHAOS – the current chaos spreading out and playing out in a divided Europe, possibly a split-up USA (with secessions), more localism and much less world trade and even interstate trade (e.g., between US states).

The energy changes will bring much pain over many years, but distributed chaos is better than a return to precivilization -- an absence of hierarchy and reduction to the elemental units of tribe and family. In the latter, society would achieve equilibrium all right -- not the one sought for, but the societal equivalent of the “heat death of the universe.”

Clayton Hallmark

Clayton Hallmark

Comments

Display the following 3 comments